The Sugar Act of 1764: The Tax Cut That Sparked a Revolution

Imagine a time when people rose up in protest of a tax being lowered. Welcome to the world of the Sugar Act.

The Sugar Act of 1764 stands as one of the most ironic moments in the history of taxation. Here Britain was actually lowering a tax, and yet colonists reacted with a fury that would help spark a revolution. To understanding this paradox, we must understand that this new act represented something far more threatening than any previous attempt by Britain to regulate its American colonies.

The Old System: Benign Neglect

For decades before 1764, Britain had maintained what historians call “salutary neglect” toward its American colonies. The Molasses Act of 1733 had imposed a steep duty of six pence per gallon on foreign molasses imported into the colonies. On paper, this seemed like a significant burden for the rum-distilling industry, which depended heavily on cheap molasses from French and Spanish Caribbean islands. In practice, though, the tax was rarely collected. Colonial merchants either bribed customs officials or simply smuggled the molasses past them. The British government essentially looked the other way, and everyone profited.

This informal arrangement worked because Britain’s primary interest in the colonies was commercial, not fiscal. The Navigation Acts required colonists to ship certain goods only to Britain and to buy manufactured goods from British merchants, which enriched British traders and manufacturers without requiring aggressive tax collection in America. As long as this system funneled wealth toward London, Parliament didn’t care much about collecting relatively small customs duties across the Atlantic.

Everything Changed in 1763

The Seven Years’ War (which Americans call the French and Indian War) changed this comfortable arrangement entirely. Britain won decisively, driving France out of North America and gaining vast new territories. But victory came with a staggering price tag. Britain’s national debt had nearly doubled to £130 million, and annual interest payments alone consumed half the government’s budget. Meanwhile, Britain now needed to maintain 10,000 troops in North America to defend its expanded empire and manage relations with Native American tribes.

Prime Minister George Grenville faced a political problem. British taxpayers, already heavily burdened, were in no mood for additional taxes. The logic seemed obvious: since the colonies had benefited from the war’s outcome and still required military protection, they should help pay for their own defense. Americans, paid far lower taxes than their counterparts in Britain—by some estimates, British residents paid 26 times more per capita in taxes than colonists did.

What the Act Actually Did

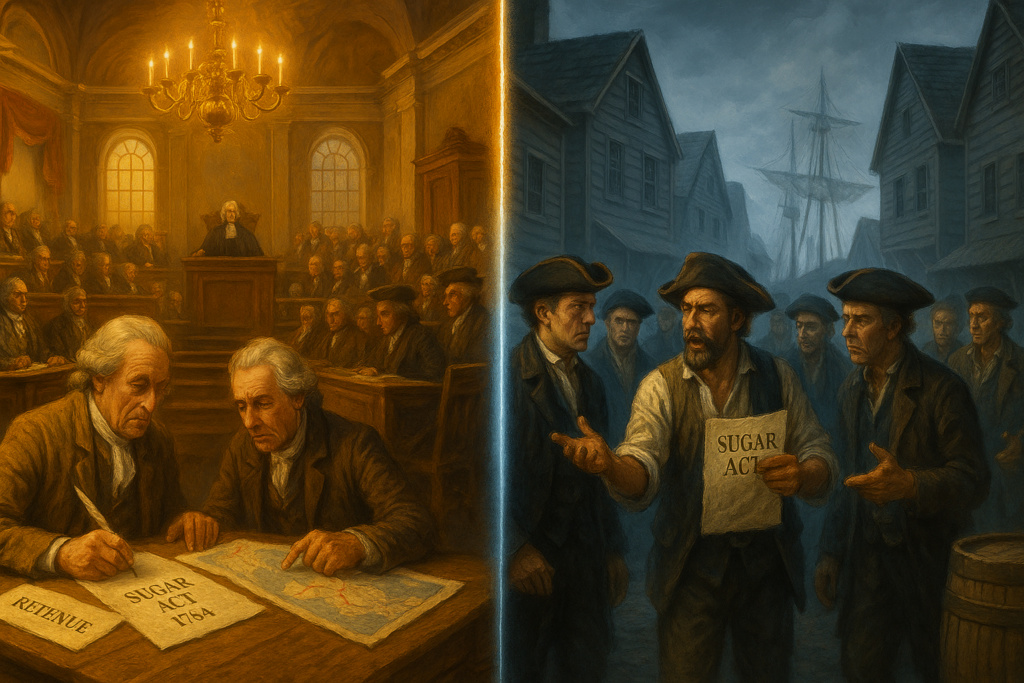

The Sugar Act (officially the American Revenue Act of 1764) approached colonial taxation differently than anything before it. First, it cut the duty on foreign molasses from six pence to three pence per gallon—a 50% reduction. Grenville calculated, reasonably, that merchants might actually pay a three-pence duty rather than risk getting caught smuggling, whereas the six-pence duty had been so high it encouraged universal evasion.

But the Act did far more than adjust molasses duties. It added or increased duties on foreign textiles, coffee, indigo, and wine imported into the colonies. colonialtened regulations around the colonial lumber trade and banned the import of foreign rum entirely. Most significantly, the Act included elaborate provisions designed to strictly enforce these duties for the first time.

The enforcement mechanisms represented the real revolution in British policy. Ship captains now had to post bonds before loading cargo and had to maintain detailed written cargo lists. Naval patrols increased dramatically. Smugglers faced having their ships and cargo seized.

Significantly, the burden of proof was shifted to the accused. They were required to prove their innocence, a reversal of traditional British justice. Most controversially, accused smugglers would be tried in vice-admiralty courts, which had no juries and whose judges received a cut of any fines levied.

The Paradox of the Lower Tax

So why did colonists react so angrily to a tax cut? The answer reveals the fundamental shift in the British-American relationship that the Sugar Act represented.

First, the issue wasn’t the tax rate. It was the certainty of collection. A six-pence tax that no one paid was infinitely preferable to a three-pence tax rigorously enforced. New England’s rum distilling industry, which employed thousands of distillery workers and sailors, depended on cheap molasses from the French West Indies. Even at three pence per gallon, the tax significantly increased operating costs. Many merchants calculated they couldn’t remain profitable if they had to pay it.

Second, and more importantly, colonists recognized that the Act’s purpose had changed relationships. Previous trade regulations, even if they involved taxes, were ostensibly about regulating commerce within the empire. The Sugar Act openly stated its purpose was raising revenue—the preamble declared it was “just and necessary that a revenue be raised” in America. This might seem like a technical distinction, but to colonists it mattered enormously. British constitutional theory held that subjects could only be taxed by their own elected representatives. Colonists elected representatives to their own assemblies but sent no representatives to Parliament. Trade regulations fell under Parliament’s legitimate authority to govern imperial commerce, but taxation for revenue was something else entirely.

Third, the enforcement mechanisms offended colonial sensibilities about justice and traditional British rights. The vice-admiralty courts denied jury trials, which colonists viewed as a fundamental right of British subjects. Having to prove your innocence rather than being presumed innocent violated another core principle. Customs officials and judges profiting from convictions created obvious incentives for abuse.

Implementation and Colonial Response

The Act took effect in September 1764, and Grenville paired it with an aggressive enforcement campaign. The Royal Navy assigned 27 ships to patrol American waters. Britain appointed new customs officials and gave them instructions to strictly do their jobs rather than accept bribes. Admiralty courts in Halifax, Nova Scotia became particularly notorious. Colonists had to travel hundreds of miles to defend themselves in a court with no jury and with a judge whose income game from convictions.

Colonists responded immediately. Boston merchants drafted a protest arguing that the act would devastate their trade. They explained that New England’s economy depended on a complex triangular trade: they sold lumber and food to the Caribbean in exchange for molasses, which they distilled into rum, which they sold to Africa for slaves, who were sold to Caribbean plantations for molasses, and the cycle repeated. Taxing molasses would break this chain and impoverish the region.

But the economic arguments quickly evolved into constitutional ones. Lawyer James Otis argued that “taxation without representation is tyranny”—a phrase that would echo through the coming decade. Colonial assemblies began passing resolutions asserting their exclusive right to tax their own constituents. They didn’t deny Parliament’s authority to regulate trade, but they drew a clear line: revenue taxation required representation.

The protests went beyond rhetoric. Colonial merchants organized boycotts of British manufactured goods. Women’s groups pledged to wear homespun cloth rather than buy British textiles. These boycotts caused enough economic pain in Britain that London merchants began lobbying Parliament for relief.

The Road to Revolution

The Sugar Act’s significance extends far beyond its immediate economic impact. It established precedents and patterns that would define the next decade of imperial crisis.

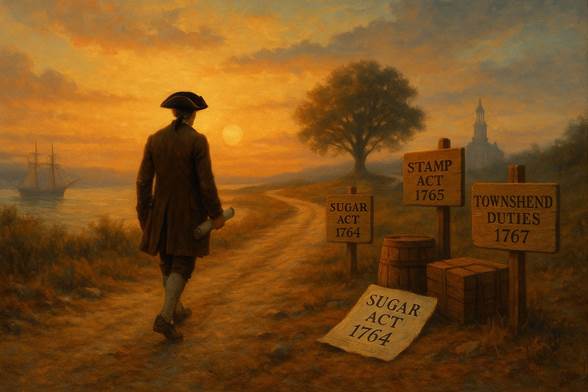

Most fundamentally, it shattered the comfortable arrangement of salutary neglect. Once Britain demonstrated it intended to actively govern and tax the colonies, the relationship could never return to its previous informality. The colonists’ constitutional objections—no taxation without representation, right to jury trials, presumption of innocence—would be repeated with increasing urgency as Parliament passed the Stamp Act (1765), Townshend Acts (1767), and Tea Act (1773).

The Sugar Act also revealed the practical difficulties of governing an empire across 3,000 miles of ocean. The vice-admiralty courts became symbols of distant, unaccountable power. When colonists couldn’t get satisfaction through established legal channels, they increasingly turned to extralegal methods, including committees of correspondence, non-importation agreements, and eventually armed resistance.

Perhaps most importantly, the Sugar Act forced colonists to articulate a political theory that ultimately proved incompatible with continued membership in the British Empire. Once they agreed to the principle that they could only be taxed by their own elected representatives, and that Parliament’s authority over them was limited to trade regulation, the logic led inexorably toward independence. Britain couldn’t accept colonial assemblies as co-equal governing bodies since Parliament claimed supreme authority over all British subjects. The colonists couldn’t accept taxation without representation since they claimed the rights of freeborn Englishmen. These positions couldn’t be reconciled.

The Sugar Act of 1764 represents the point where the British Empire’s century-long success in North America began to unravel. By trying to make the colonies pay a modest share of imperial costs through what seemed like reasonable means, Britain inadvertently set in motion forces that would break the empire apart just twelve years later.

Sources

Mount Vernon Digital Encyclopedia – Sugar Act https://www.mountvernon.org/library/digitalhistory/digital-encyclopedia/article/sugar-act/ Provides overview of the Act’s provisions, economic context, and relationship to British debt from the Seven Years’ War. Includes information on tax burden comparisons between Britain and the colonies.

Britannica – Sugar Act https://www.britannica.com/event/Sugar-Act Covers the specific provisions of the Act, enforcement mechanisms, vice-admiralty courts, and the shift from the Molasses Act of 1733. Useful for technical details of the legislation.

History.com – Sugar Act https://www.history.com/topics/american-revolution/sugar-act Discusses colonial constitutional objections, the “taxation without representation” argument, and the enforcement provisions including burden of proof reversal and jury trial denial.

American Battlefield Trust – Sugar Act https://www.battlefields.org/learn/articles/sugar-act Details colonial response including boycotts, James Otis’s arguments, and the triangular trade system that the Act disrupted.

Additional Recommended Sources

Library of Congress – The Sugar Act https://www.loc.gov/collections/continental-congress-and-constitutional-convention-broadsides/articles-and-essays/continental-congress-broadsides/broadsides-related-to-the-sugar-act/ Primary source collection including contemporary colonial broadsides and protests against the Act.

National Archives – The Sugar Act (Primary Source Text) https://founders.archives.gov/about/Sugar-Act The actual text of the American Revenue Act of 1764, useful for verifying specific provisions and language.

Yale Law School – Avalon Project: Resolutions of the Continental Congress (October 19, 1765) https://avalon.law.yale.edu/18th_century/resolu65.asp Colonial responses to the Sugar and Stamp Acts, showing how the arguments evolved.

Massachusetts Historical Society – James Otis’s Rights of the British Colonies Asserted and Proved (1764) https://www.masshist.org/digitalhistory/revolution/taxation-without-representation Primary source for the “taxation without representation” argument that emerged from Sugar Act opposition.

Colonial Williamsburg Foundation – Sugar Act of 1764 https://www.colonialwilliamsburg.org/learn/deep-dives/sugar-act-1764/ Discusses economic impact on colonial merchants and the rum distilling industry.

Supply-Side Economics and Trickle-Down: What Actually Happened?

By John Turley

On January 12, 2026

In Commentary, Politics

The Basic Question

You’ve probably heard politicians arguing about tax cuts—some promising they’ll supercharge the economy, others dismissing them as giveaways to the rich. These debates usually involve two terms that get thrown around like political footballs: “supply-side economics” and “trickle-down economics.” But what do these terms actually mean, and more importantly, do they work? After four decades of real-world experiments, we finally have enough data to answer that question.

Understanding Supply-Side Economics

Supply-side economics is a legitimate economic theory that emerged in the 1970s when the U.S. economy was struggling with both high inflation and high unemployment—a combination that traditional economic theories said shouldn’t happen. The core idea is straightforward: economic growth comes from producing more goods and services (the “supply” side), not just from boosting consumer demand.

The theory rests on three main pillars. First, lower taxes—the thinking is that if people and businesses keep more of their money, they’ll work harder, invest more, and create jobs. According to economist Arthur Laffer’s famous curve, there’s supposedly a sweet spot where lower tax rates can actually generate more government revenue because the economy grows so much. Second, less regulation removes government restrictions so businesses can innovate and operate more efficiently. Third, smart monetary policy keeps inflation in check while maintaining enough money in the economy to fuel growth.

All of this sounds reasonable in theory. After all, who wouldn’t work harder if they kept more of their paycheck?

The Political Rebranding: Enter “Trickle-Down”

Here’s where economic theory meets political messaging. “Trickle-down economics” isn’t an academic term—it’s essentially a catchphrase, and not a complimentary one. Critics use it to describe supply-side policies when those policies mainly benefit wealthy people and corporations. The idea behind the name: give tax breaks to rich people and big companies, and the benefits will eventually “trickle down” to everyone else through job creation, higher wages, and economic growth.

Here’s the interesting part: no economist actually calls their theory “trickle-down economics.” Even David Stockman, President Reagan’s own budget director, later admitted that “supply-side” was basically a rebranding of “trickle-down” to make tax cuts for the wealthy easier to sell politically. So while they’re not identical concepts, they’re two sides of the same coin.

The Reagan Revolution: Testing the Theory

Ronald Reagan became president in 1981 and implemented the biggest supply-side experiment in U.S. history. He slashed the top tax rate from 70% down to 50%, and eventually to just 28%, arguing this would unleash economic growth that would lift all boats.

The results were genuinely mixed. On one hand, the economy created about 20 million jobs during Reagan’s presidency, unemployment fell from 7.6% to 5.5%, and the economy grew by 26% over eight years. Those aren’t small achievements.

But the picture gets more complicated when you look deeper. The tax cuts didn’t pay for themselves as promised—they reduced government revenue by about 9% initially. Reagan had to backtrack and raise taxes multiple times in 1982, 1983, 1984, and 1987 to address the mounting deficit problem. Income inequality increased significantly during this period, and surprisingly, the poverty rate at the end of Reagan’s term was essentially the same as when he started. Perhaps most telling, government debt more than doubled as a percentage of the economy.

There’s another wrinkle worth mentioning: much of the economic recovery happened because Federal Reserve Chairman Paul Volcker had already broken the back of inflation through tight monetary policy before Reagan’s tax cuts took effect. Disentangling how much credit Reagan’s policies deserve versus Volcker’s groundwork is genuinely difficult.

The Pattern Repeats

The story didn’t end with Reagan. George W. Bush enacted major tax cuts in 2001 and 2003, especially benefiting wealthy Americans. The result? Economic growth remained sluggish, deficits ballooned, and income inequality continued its upward march.

Then there’s Bill Clinton—the plot twist in this story. In 1993, Clinton actually raised taxes on the wealthy, pushing the top rate from 31% back up to 39.6%. Conservative economists predicted economic disaster. Instead, the economy boomed with what was then the longest sustained growth period in U.S. history, creating 22.7 million jobs. Even more remarkably, the government ran a budget surplus for the first time in decades.

Donald Trump’s 2017 tax cuts, focused heavily on corporations, showed minimal wage growth for workers while generating significant stock buybacks that primarily benefited shareholders—and yes, larger deficits. Trump’s subsequent economic policies in his second term have been characterized by such volatility that reasonable long-term assessments remain difficult.

The Kansas Experiment: A Modern Test Case

At the state level, Kansas Governor Sam Brownback implemented one of the boldest modern experiments in supply-side policy between 2012 and 2017, dramatically slashing income taxes especially for businesses. Proponents called it a “real live experiment” that would demonstrate supply-side principles in action.

Instead of unleashing growth, Kansas faced severe budget shortfalls that forced cuts to education and infrastructure. Economic growth actually lagged behind neighboring states that didn’t implement such aggressive cuts, and the state legislature eventually reversed many of the tax reductions. This case has become a frequently cited cautionary tale for critics of supply-side policies.

What Does Half a Century of Data Show?

After 50 years of real-world experiments, researchers finally have enough data to move beyond political rhetoric. A comprehensive study analyzed tax policy changes across 18 developed countries over five decades, looking at what actually happened after major tax cuts for the wealthy.

The findings are remarkably consistent. Tax cuts for the rich reliably increase income inequality—no surprise there. But they show no significant effect on overall economic growth rates and no significant effect on unemployment. Perhaps most damaging to the theory, they don’t “pay for themselves” through increased growth. At best, about one-third of lost revenue gets recovered through expanded economic activity.

In simpler terms: when you cut taxes for wealthy people, wealthy people get wealthier. The promised broader benefits largely fail to materialize. The 2022 World Inequality Report reinforced these conclusions, finding that the world’s richest 10% continue capturing the vast majority of all economic gains, while the bottom half of the population holds just 2% of all wealth.

Why the Theory Doesn’t Match Reality

When you think about it logically, the disconnect makes sense. If you give a tax cut to someone who’s already wealthy, they’ll probably save or invest most of it—they were already buying what they wanted and needed. Their daily spending habits don’t change much. But if you give money to someone who’s struggling to pay bills or afford necessities, they’ll spend it immediately, directly stimulating economic activity.

Economists call this concept “marginal propensity to consume,” and it explains why giving tax breaks to working and middle-class people actually does more to boost the economy than supply-side cuts focused on the wealthy. A dollar in the hands of someone who needs to spend it has more immediate economic impact than a dollar added to an already-substantial investment portfolio.

The Bottom Line

After 40-plus years of repeated experiments, the pattern is clear. Supply-side policies and trickle-down approaches consistently increase deficits, widen inequality, and fail to significantly boost overall economic growth or create more jobs than alternative policies. Meanwhile, periods with higher taxes on the wealthy, like the Clinton years, saw strong growth, robust job creation, and balanced budgets.

The Nuance Worth Keeping

None of this means all tax cuts are bad or that high taxes are always good—economics is rarely that simple. The critical questions are: who receives the tax cuts, and what outcomes do you realistically expect? Targeted tax cuts for working families, small businesses, or specific industries facing genuine challenges can serve as effective policy tools. Child tax credits, research and development incentives, or relief for struggling sectors might accomplish specific goals.

But the evidence accumulated over four decades is clear: broad tax cuts focused primarily on the wealthy and large corporations don’t deliver the promised economic benefits for everyone else. The benefits don’t trickle down in any meaningful way.

You’ll keep hearing these arguments for years to come. Politicians will continue promising that tax cuts for businesses and the wealthy will boost the entire economy. Now you know what the actual evidence shows, and you can judge those promises accordingly.

Sources: